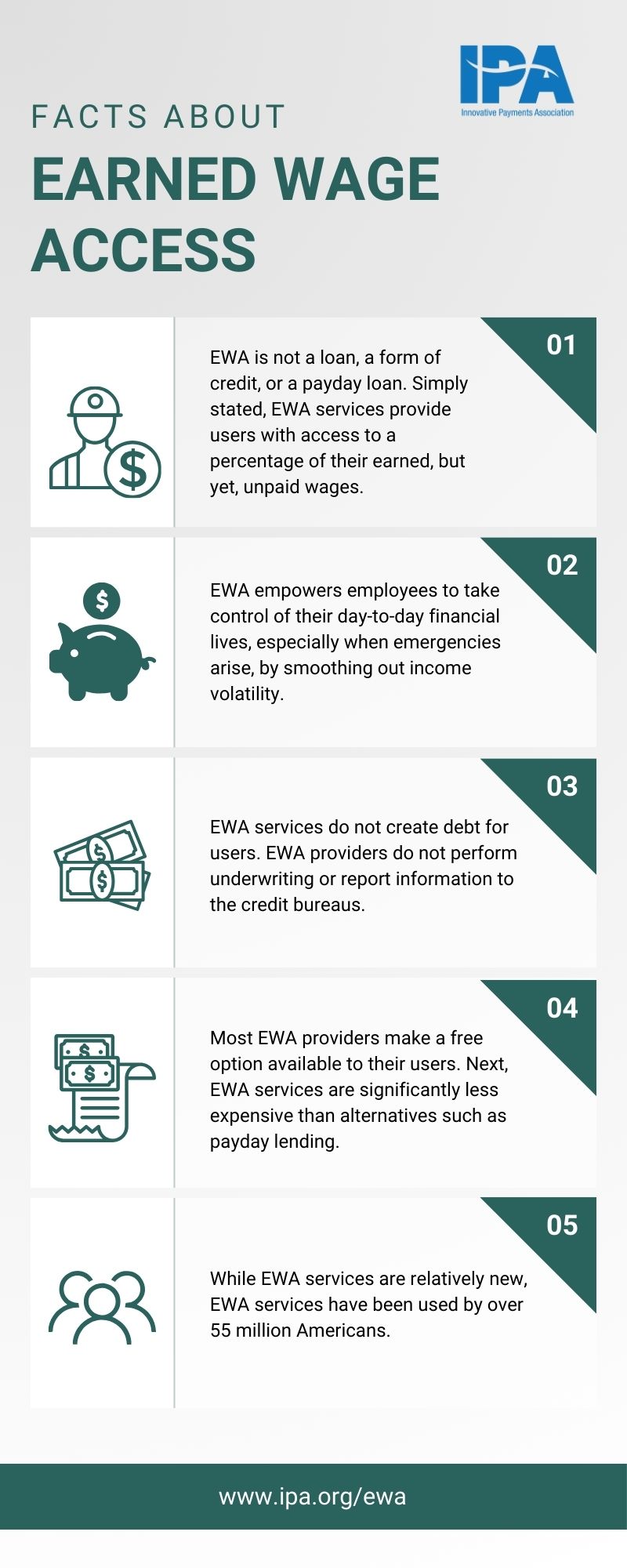

Earned Wage Access (EWA) services have quickly emerged as a valuable tool to aid American workers in managing financial strain and budgeting. Working Americans are in the best position to determine when they must access the money they have earned but have not yet been paid due to the timing of wage payments – which are decided by employers. EWA allows employees to gain greater control over their own financial lives without having to rely on more costly alternatives like traditional payday loans or overdraft programs.

According to the Financial Health Network’s April 2022 report on EWA, many EWA services cost consumers an average of $2.59 to $6.27 per transaction – while costs for alternative products are significantly higher. For example, the average overdraft fee is $35; title and payday loan fees range from $15 to $100; and pawn loan fees range from $75 to $100. The need for EWA is demonstrated by research that shows that income volatility can lead to poverty for families. EWA can help smooth out income flows, as demonstrated by a survey from the Financial Health Network. It found that 37% of low-wage workers say they “worry about running out of food before getting money to buy more.”

{kind=link}